Car & Motor Insurance

What Is Car Insurance?

With over 400,000 recorded road accidents in 2010 along with how cars are becoming indispensible assets, getting a good insurance policy has never been more important to protect not just yourself and your car, but the other parties who may be involved in accidents.

An insurance policy will protect the driver from bearing all the financial burden in the event of an accident, in exchange for an annual insurance premium.

- Third party cover - This policy insures you against claims made against you for bodily injuries or deaths caused to other persons (known as the third party), as well as loss or damage to third party property caused by the use of your vehicle.

- Third party, fire and theft cover - This policy provides insurance against claims for third party bodily injury and death, third party property loss or damage, and also accidental loss or damage to your own vehicle due to fire or theft.

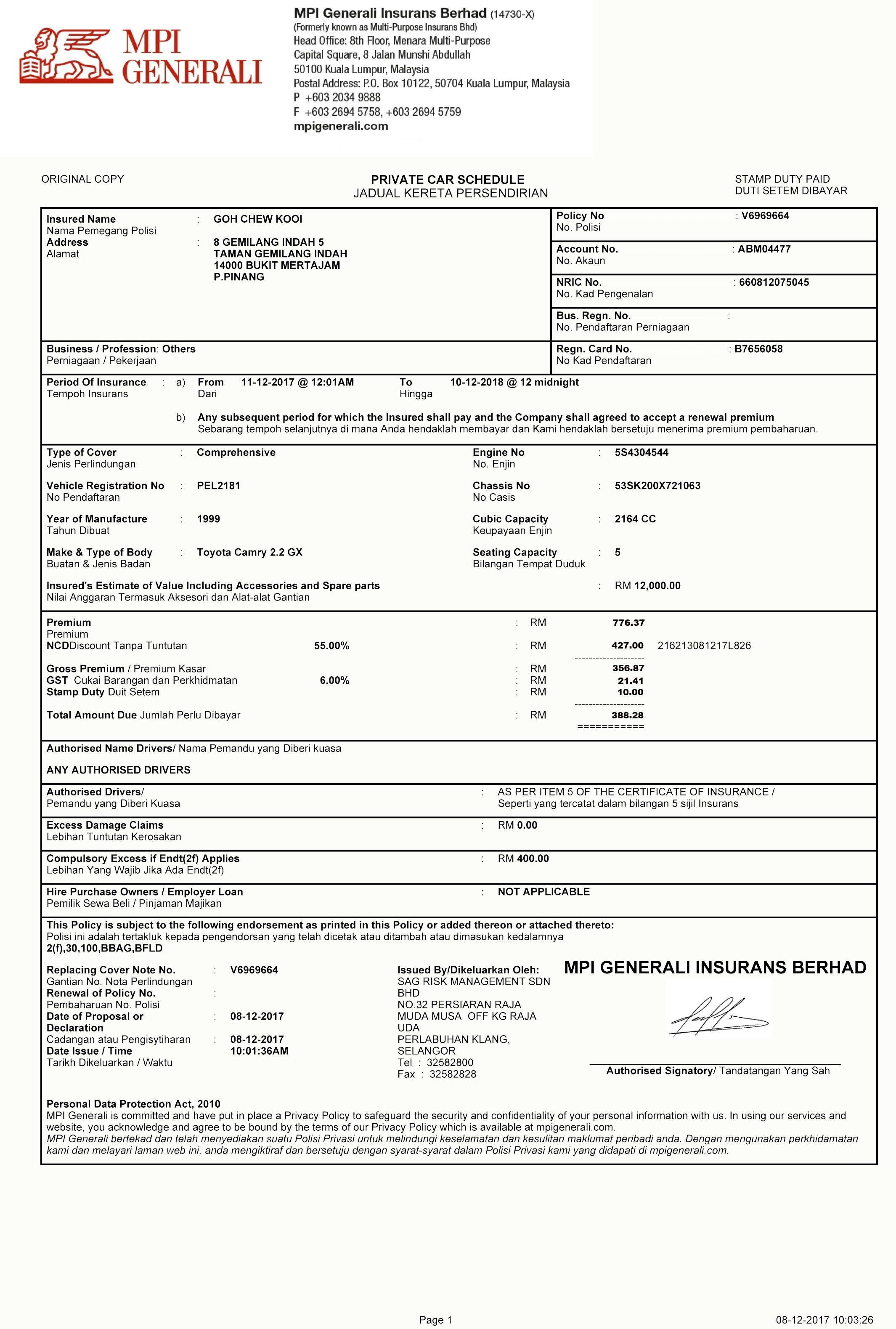

- Comprehensive cover - This policy provides the widest coverage, i.e. third party bodily injury and death, third party property loss or damage and accidental loss or damage to your own vehicle due to fire, theft or damage to your own vehicle.

By paying additional premium, you can add on the following benefits:

- Windscreen Damage

- Passenger’s liability cover

- Legal liability of passengers

- Damage arising from floods, landslide and storms

- Loss or damage to NGV tank

- Loss or damage to vehicle accessories

- NCD relief extension

- Compensation for assessed repair time

- Strikes, riots and civil commotion cover

- Geographical area extension - Thailand

- Geographical area extension – West Kalimantan

The factors affecting the base premium of car insurance are Location, Total Insured Value of a car (depends on market value) and Cubic Capacity of a car. The pricing of premiums is mostly tariffed by the Bank Negara Malaysia and the General Insurance Association of Malaysia.

- Location

The base value will be affected by whether the car is in East or West Malaysia

- Total Insure Value

The total value of which you are going to insure your vehicle for. It is acceptable to over insure or under insure your car.

Undervaluing your car will result in the insurance company compensating for up to the amount insured. Any additional costs will be considered as self-insured or borne by the owner.

Overvaluing your car will result in higher premiums with the insurance company only compensating for the market value for the car.

- Cubic Capacity

The size of your engine

Drivers have access to No-Claim Discount if the driver has not claimed from their policy for previous years. This discount rate is regulated by the Bank Negara Malaysia and the General Insurance Association of Malaysia. No-claim discounts can reduce premium amounts by up to 50 percent.

There are factors known as Loading that will increase the premium needed for insurance. These are factors that influence the risk an insurance company has for a car.

- Age of Driver

Drivers aged less than 26 and above 69.

- Age of Car

Cars above the age of 10.

- Claims Experience

Frequency of claims made.

- Reconditioned /Second Hand Vehicles

Adjusters will evaluate the condition of reconditioned / second hand cars.

- High-Performance / Sports Vehicles

High performance/sports vehicles will incur additional Loading.

- High Risk Theft Vehicle (HRTV)

Cars listed in the HRTV list will incur additional Loading.

- Windshield Insurance

In the event your windshield gets damaged, this cover provides insurance for repairs or replacement without affecting your No-Claim Discount.

- Audio and Accessories Cover

In the event your car accessories are damaged, this cover provides insurance for repairs or replacement without affecting your No-Claim Discount.

- Special Perils

In the event your car is damaged by acts of nature such as Floods, Landslides, earthquakes, etc, your car is covered.

- Number of Authorized Drivers

A premium will be incurred for increased number of drivers in the policy.

- Number of Seats

A premium will be charged for cars with more than 5 seats.

- Gas Conversion Kit and Tank

This is to cover for Natural Gas Vehicle kit and tanks.

- Legal Liabilities to Passengers

Used in the event the passengers from your car sues you for negligence.

- Legal Liabilities of Passengers

Used in the event to cover legal liabilities of your passengers for negligence.

- Compensation for Assessed Repair Time

Compensation for time your car is in the workshop for repairs.

Insurance companies may incur additional Loading from a driver’s history to compensate for the risk borne by them

- Select Insurance Menu, click Request Insurance Quotation

- Fill up Insurance’s info , decide any discount to customer and whether customer needs road tax (if yes, provide mailing address) . Click “Choose File” button , snap a picture of the registration card/cover note.

- Fill out owner info and car info,

Important: 1) Customer Name 2) IC Number 3) Number Plate 4) Chassis No/Engine No - Click Next

- Double check the fill owner info and car info before do the submission by clicking submit button.

- Select which your prefer quotation after do survey

-

To upload payment slip : click payment slip and named Insurance company, amount , bank and upload payment proof screenshot.

- Cover Note / E-Policy issued within 2-3 working hours in PDF and email /sms immediately to customer